An SDLT supplement

March Tax Technical Update by Lakshmi Narain

The Chancellor confirmed that the proposals, announced in the autumn statement on the 25th November 2015, would proceed. Indeed, further significant SDLT changes were announced relating to commercial properties.

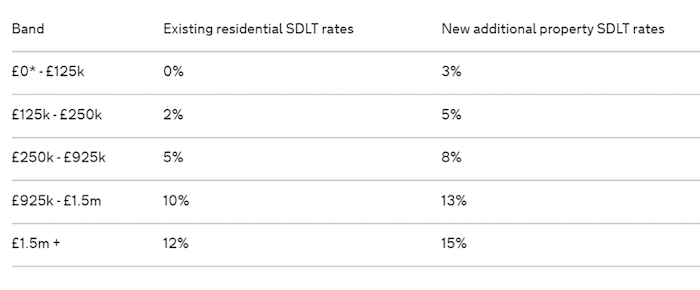

The SDLT supplement (or surcharge as it is also known as) is to be set at 3% and will apply from 1 April 2016 (with some transitional rules which I will not deal with here). The proposals set out in the Consultation document published on the 28th December are to be implemented broadly. There has been some modification of the proposals, and there will be a need to look closely at the legislation as it makes its way through the parliamentary process, to see whether some of the concerns expressed by the professional bodies is heeded. The rate structure for residential properties in England and Wales and Northern Ireland is:

It should be noted that SDLT does not apply to properties in Scotland. Scotland has its own Land and Buildings Transaction Tax (LBTT): they have implemented legislation that is very similar to that in the Finance Bill 2016.

Broadly, the charge applies where, at the end of the day on which the transaction is completed, the purchaser has two or more residential property interests. However, no charge will apply if the property being acquired is either replacing, or is to replace the person's main residence (within 18 months).

This is neatly summarised by the flowchart published in the response document:

.png)

There was a suggestion that the charge would not apply to companies and may not apply to "bulk" purchasers or large scale investors. The latter two, it was suggested, would need to meet a 15 property test.

The main modifications to the original proposals are that the 18-month test is now to be a 36-month test (a little bizarre as the 18-month test continues for CGT relief for the final period of ownership), and that there would be no relief for bulk purchasers' large scale investors. Further, the 36-month time period will commence from 25 November 2015, for those who had sold a previous main residence prior to that date.

Purchasers with more than one property who dispose of a main residence, have 36 months to buy a new main residence before the higher rates apply assuming they retain their additional property. Further, in the event that purchasers are subject to the higher rates of SDLT because they buy a new main residence before disposing of their previous main residence, they are entitled to a refund from the higher rates of SDLT if they dispose of their previous main residence within 36 months

The government has also decided that married couples who are living separately in circumstances that are likely to become permanent will not be treated as one unit for the purposes of this policy. This will, therefore, allow for situations where couples had separated but had chosen not to divorce formally. Further, when applying the higher rates, a small share (50% or less) in a single property which has been inherited within the 36 months prior to the transaction will not be considered as an additional property. This is intended to provide flexibility for purchasers who may find it difficult to dispose of a share in a property quickly.

There are a number of technical issues that are being discussed (for example the application of what is referred to as the linked transactions rules) and we will need to see how those discussions progress.

What next?

There appears to be a clear and sustained attack on the residential property investment sector with the implementation of an SDLT supplement, the proposal (from April 2017) to phase in the reduction of income tax relief for financing costs, the removal (from April 2016) of the wear and tear allowance and the introduction of a furnishings replacement relief. It is also worth noting that the proposal to reduce the rates of CGT for individuals from 28% / 18% to 20% /10% from April 2016 was qualified by declaration that this would not apply to certain gains (such as on property disposals) there would be an 8% surcharge.

With the reduction in CGT, the introduction of the £5,000 dividend allowance and the extension of the 10% rate to a new entrepreneur’s relief, there may be an incentive for individuals to reconsider their investment portfolio.

If you have any comments or questions relating to the comments in this blog, please feel free to get in contact. Next month, I will look further at the changes to CGT and, in particular, to Entrepreneur’s Relief.